I had heard a commercial on the radio pitching "return of premium" life insurance. This was a fast-paced, boisterous commercial - indistinguishable from low end mortgage pitches - that promised to return all your yearly premiums at the end of the term. I thought this sounded too good be true - there had to be a catch they weren't telling you about - so I forgot about it.

A few months later I read an article in Forbes about ROP insurance policies - and the magazine gives them a resounding thumbs up. Assuming you live through your term.

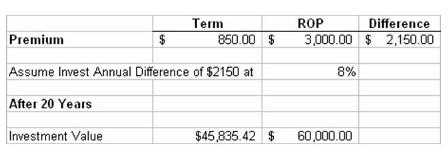

This is how Forbes analyzes them: ROP policies are more expensive than standard term policies. If you take the equivalent term policy and assume you invest the difference, you can quickly calculate if the ROP is a good deal.

So I gave it a shot. I ran through two scenarios on lifeinsurance.com using the same term and payout:

So at the end of 20 years, the ROP would give me back all my premiums, or $60K. If I take the term insurance and invest the difference - and got an fairly good 8% return - I wouldn't match what I got on the ROP.

So it looks like ROP is the way to go. Of course this assumes you live all 20 years. If you die first, then it's a bad deal since you paid out much higher premiums for the same amount of coverage - and of course you won't get your premiums back.

No comments:

Post a Comment